Social Security COLA for 2022 Could Be Biggest since 2009 or even 1982, But Wont Cover Cost Increases for Many Retirees

by Wolf Richter Aug 11, 2021

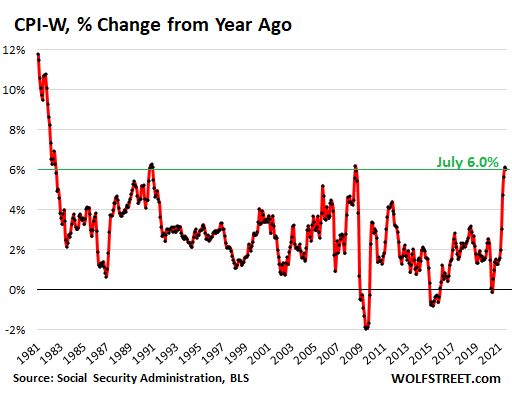

Its based on CPI-W for the third quarter. July came in at 6.0%.

By Wolf Richter for WOLF STREET.

One of the inflation measures released today, in addition to the regular Consumer Price Index data, was the CPI-W which is used to figure the Cost of Living Adjustment (COLA) for Social Security benefits.

The COLA is based on the average percentage increase of CPI-W in the third quarter compared to the same period in the prior year. So todays report for July, figured by the Bureau of Labor Statistics and released by the Social Security Administration, covers the first month of the three months that will determine the Social Security COLA applied to benefits paid in the year starting in January 2022.

The CPI-W for July jumped by 6.0% year-over-year, following the June increase of 6.1%. Both were the biggest since July 2008 (6.2%). All three of them were the biggest since November 1990 (6.3%).

In contrast to the increase in the CPI-W of 6.0% for July and 6.1% for June, the regular CPI (the CPI-U), rose 5.4% for both months.

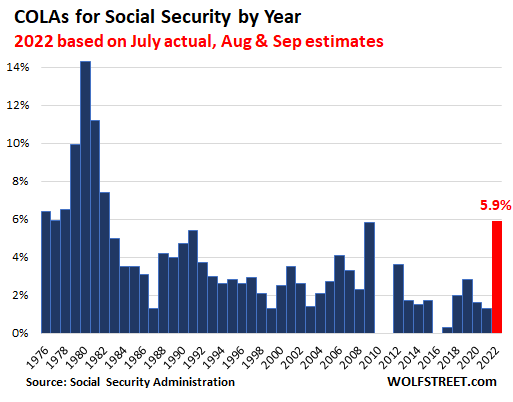

The average year-over-year increase of July, August, and September will determine the COLA applied to Social Security benefits paid in 2022.

For example, if the CPI-W for August rises 5.9% and for September 5.8%, the average year-over-year increase in Q3 would be 5.9%, and the COLA for 2022 would also be 5.9%.

Using these estimates for August and September, it would produce the highest Social Security COLA since 1982 (7.4%). In recent memory, the highest COLA was 5.8% in 2009. The September value of CPI-W, to be released in about two months, will allow us to predict with some accuracy the COLA for 2022.

A COLA of around 6% might sound exciting, but given the extent to which prices are rising, 6% might not even get close to making up for actual cost increases, depending on the personal situation of the beneficiary.

If you get hit with a 10% rent increase, and the price of gasoline jumps another 30%, and the stuff you buy at the supermarket is up 8%, then the COLA wont be nearly enough. In other situations, you might fare better.

But given how suppressed housing costs and new and used vehicle costs and other costs are in the regular CPI (which I discuss here), these COLAs over time will not compensate for the actual increases in the costs of maintaining the current standard of living. This is why its super important to have a nest egg with at least some assets to supplement Social Security.

And having a fun and exciting gig for as long as possible that generates income is a huge benefit for all kinds of reasons, not just money, or maybe least of all money. I mean, look at all the old politicians: Theyre having a total blast. They get to be on TV, give speeches, and play beach volleyball with trillions of dollars, and get paid to do it. Way to go!

https://wolfstreet.com/2021/08/11/so...many-retirees/

Reply With Quote

Reply With Quote